Today I will talk about the simplest financial product known to me – the Recurring Deposit or RD as it is called. Most investors know about Recurring Deposits and have used them at some point of time. However, many investors are still confused regarding this straightforward product.

Also, I will share tips on extracting the maximum benefit out of Recurring Deposits and on using this product to lead a better financial life. (Even our upcoming investors bootcamp will help you lead a better financial life).

Simple and Beautiful financial Product

Recurring Deposits are often rightfully called one of the simplest financial products in the world. You open a Recurring Deposit for a fixed amount and for a fixed tenure. Each month that fixed amount is invested and you earn interest (at a predefined rate) on the Recurring Deposit.

For example – You can open a Rs. 1,000 Recurring Deposit for 2 years @ 9% interest. Now for the next 24 months, Rs. 1,000 will be invested from your bank account and it will get accumulated in the Recurring Deposit and will accrue interest at the rate that was offered. This is exactly the same as putting Rs. 1,000 in a piggy bank on a certain date for the next 2 years, except that in Recurring Deposit you also get interest income (which is not an option with the piggy bank).

I have been unequivocal in stating that almost all new investors who enter the world of personal finance should start with Recurring Deposits. Typically, new investors do not fully understand the principles behind personal finance and so to protect their money from the they leave funds dormant in their savings account or use them up for some other purpose. Instead, by creating a Recurring Deposit, they will ensure their income is getting channeled into investments and more importantly that they earn interest on their money – eventually leading to good investing habits being formed. Gradually over the next 1-2 years, they can start investing in other instruments such as mutual funds, real estate or bonds.

Planning your Short Term Goals using Recurring Deposits

A Recurring Deposit is a safe investment, or in other words, it is a financial product with guaranteed returns. Stocks or mutual funds are not ideal investments for short tenures. There isno guaranteed return in equity-based productsand consistent returns can only be expected over a long horizon of 8-10 years.

Recurring deposits are therefore the ideal products to consider when planning short-term goals over a horizon of 1-3 yrs. These may include

- A corpus for a downpayment of our new home

- Education fees for your children (yearly fees paid in one shot)

- Home Renovation expenses

- Higher Education Expenses if you are in Job

- Upcoming Marriage expenses due in 2-3 years (e.g. sister’s/brother’s marriage)

- Setting aside funds for a vacation

Now if you look at most of these goals above, Recurring Deposits give returns similar to those of Fixed Deposits. Returns are at the moment in the range of 8-10% depending on the tenure chosen. As Recurring Deposits do not carry risk, they are the ideal investment solution for short-term goals (such as the ones above) where the investor is looking for guaranteed and liquid returns on savings.

Using Recurring Deposits for Ultra Short term goals in life

But the real reason why I love Recurring Deposits the most is this – Recurring Deposits are without doubt, the most powerful way to reach your ultra short-term goals in life. The parts below are excerpted from my 2nd book – “How to be your own financial planner in 10 steps“.

How many long-term financial goals do you have in life – A maximum of 3 or 4, right? Investors tend to overemphasize their focus on this handful of goals in life and spend most of their time working towards them. However most of these goals are so distant in the future, that planning for them is virtually impossible. On the other hand, we have dozens of small goals in life, which are due in next 6 or 8 months or a year at the most. We really aspire to achieve these goals, but ironically, never plan for them – because we think they can be achieved without planning.

Let me explain -

Imagine you want to buy Nokia ‘Lumia 720’ in the coming 6 months. This is very small goal. But most people think about it and leave it hoping to have sufficient money for the phone when the time comes. Now imagine 8 months go by. If at that time, the person has enough money in his account, the idea to buy the phone will again occur to him and he will make the purchase. And if the money is not there, the purchase idea yet again gets pushed out in to the future.

The same habit recurs in a case where you might wish to gift a small vacation to your parents on their birthday next year. Lets say you want to send your parents on a small vacation after a year, and it would cost Rs. 25,000. Now again no one “plans” for it. The matter of having sufficient funds when the time comes is left to chance.

Now here comes the power of Recurring Deposits where you convert each ‘small expenditure’ that is due in the next 6 months to 2 years (not more than this please) into a goal – and open a Recurring Deposit for it. You then let the money flow out of your bank account each month without manually getting involved, set reminders for each goal on the target date and keep achieving those goals!

Example of using Recurring Deposits in a Scenario

Imagine you have 3 small goals within next 1.5 years and those are

- Buy Nokia Lumia 720 in next 10 months – Rs 20,000

- Gift a Vacation to Parents in next 1 yr – Rs 25,000

- Pay Installment of you Kid Pre-school in next 1 yr – Rs 25,000

Most people have goals similar to the ones listed above. To achieve these goals, you can open 3 Recurring Deposits (one for each of these), for the exact tenure (10 months, 1 year and 1.5 years). Consequently, just by having small investments each month, your planning for short-term goals will become quite robust. As the deposits mature, you will find that you have the financial means to achieve your goals without scrabbling to arrange money at the last moment or worse, having to drop your goals altogether.

Taking the above example, The RD’s would be like this

- Buy Phone – Start 10 months RD for Rs 2,000

- Gifting Vacation – Start 1 yr RD for Rs 2,000

- Pre-school Fees – Start 1 yr RD for Rs 2,000

- Total Money going in RD each month – Rs 6,000

What you have done above is to give concrete shape to your short- term goals by using Recurring Deposits and prevent your goals from turning into perennially postponed wishes or wishes that remain unfulfilled throughout your life.

Simplicity means Fast Action

Setting up a Recurring Deposit is so easy it’s almost effortless. You can log onto your Internet-banking page and open an online Recurring Deposit within seconds. You just have to pick the amount per month, the tenure and the date you want the money to be debited from your bank account – and your Recurring Deposit is all set. This simplicity in setting up also helps you take actions faster

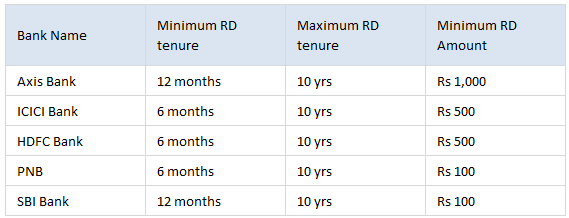

Recurring Deposits Tenure’s and minimum Requirement

The minimum and maximum tenure and amount for recurring deposits varies from one bank to the other. In general, PSU banks such as SBI Bank, PNB or Andhra Bank have a minimum limit of Rs. 100 to open a recurring deposit. However, private banks such as ICICI, HDFC or Axis have minimum limits of Rs. 500 or Rs. 1000. The maximum tenure for Recurring Deposits is up to 10 yrs. Here is a snapshot just to give you an idea

Some other Features of Recurring Deposits

- There is no TDS applicable on recurring deposits, but the interest income is fully taxable in your hands.

- You can break your recurring deposits anytime before maturity with some penal interest. The interest applicable will be the rates applicable for the tenure RD was running and not the original tenure chosen.

- Some Banks offer flexi recurring deposits also, where you can increase the amount of deposit each month (but cant decrease it)

- The minimum tenure for RD is 6 months and maximum is 10 yrs

- You can start recurring deposits for minimum of Rs 500 or Rs 1,000 . In post office its minimum Rs 10

- Recurring deposits comes with Nomination Facility, so your nominee will be contacted and handed over the money if you die.

- You can take loans against your recurring deposits for 80-90% of RD worth

- Interest is compounded on quarterly basis in recurring deposits

Please share what you think about Recurring Deposits. Have you used them? Can you share one insight or hidden information about Recurring Deposits, which you feel may help others!

0 comments:

Post a Comment